- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

The Physician on FIRE Investment Portfolio

This is how one physician invests his money, applying a chosen asset allocation across mulitple accounts. I provide a rationale for the allocation and placement of funds within each account.

I’ve touched on the importance of investing early and often, but I haven’t given you a clue as to how I invest. It wasn’t until sometime last year that I wrote myself an Investor Policy Statement and came up with an asset allocation that felt appropriate. I made a few transactions to apply the allocation across my various accounts. This is the allocation I’ve decided upon:

• 60% US Stocks (with a tilt to small and value)

• 20% International Stocks (50/50 developed and emerging markets)

• 10% REIT (Real Estate Investment Trust)

• 10% Bond & Cash (mostly bond plus cash emergency fund)

Is this the perfect asset allocation?

No. The White Coat Investor has identified 150 other asset allocations that are “better than yours,” although I think mine is definitely better than some of them. The only way to know, of course, is to look back at some future date and determine which portfolio performed the best. We could look in the rearview mirror and backtest a bunch of portfolios, but as we all know, past performance does not predict future results.

How did I come up with this allocation?

I read a couple books, spent some time exploring Bogleheads and other websites, and determined my risk tolerance. Vanguard has a simple risk tolerance questionnaire that takes a couple minutes to complete. Researching for this post, I played around with it a little bit and couldn’t actually come up with a 90/10 stock bond recommendation. I’m not sure that outcome is even in the algorithm. I usually got 100% stock or 80/20 or 70/30 depending on when I said I would start taking the money from my investments.

The majority of my portfolio is invested in US stocks. I like stocks for the returns, which have delivered an average of about 10% a year for a very long time. Small and value stocks are favored by people smarter than me for potentially higher returns, so I tilt a bit that way.

I have international stocks for diversification. I overweight emerging markets for the same reason I tilt to small value. Experts with much more experience than me recommend anywhere from 0% to 50% or more of your stock portion be international. I’ve gone with a nice round number in the middle.

REIT funds are considered part of the stock portion, but provide some additional diversity. High volatility has been rewarded with solid returns, particularly if you look back more than 10 years. That says nothing about the future, but real estate will always be required by businesses and people.

Bonds are there as a safe haven and diversifier. If we experience a downturn worse than the Great Depression, I should have something left. I doubt that will happen, but I feel better having a small bond allocation than none at all.

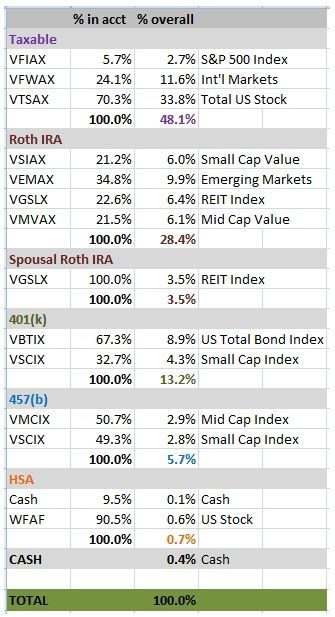

Let’s look under the hood.

Here is what my asset allocation looks like as actually applied in my various accounts.

The PoF Portfolio in Action

The taxable account has US stocks and International stocks. I tax loss harvest from this account, so the particular fund(s) used will vary as I exchange from one fund to a similar fund.

The Roth accounts have my small-cap and mid-cap value stocks, emerging markets, and REIT. The REIT fund is not very tax efficient, so this is a good place for it.

You might wonder how I have such a large percentage in the Roth IRA. Back in 2010, I converted pretty much all my retirement savings, which was in a SEP-IRA, to Roth. In hindsight, it was probably not the smartest move, but the prevailing thought at the time was that the window to make a conversion would only be open to high earners for one year. The window never closed, and I paid six figures in extra income tax by making the conversion when I did. Live and learn.

I keep bonds in the 401(k). A total bond fund is not particularly tax efficient, so this is a good place for my bonds. After I retire, I anticipate rolling this over to a traditional IRA, and likely doing some Roth conversions. Whatever hasn’t been converted when I turn 70 will be subject to RMDs, so I also like bonds here for the likely lower long-term return.

The 457(b) has small-caps and mid-caps. Since I tax loss harvest in the taxable account, I avoid keeping identical funds here or anywhere else in the portfolio. Automatic investment and reinvestment of dividends could trigger a wash sale. The 457(b) fund will start paying out the year after I retire. I will eventually put some bonds in here since this will be part of the portfolio that I will be spending from in early retirement.

Nearly all funds are with Vanguard, with the exception of my HSA, where options are limited. Vanguard has low expenses and a great track record. The portfolio consists entirely of mutual funds and a small amount of cash. I could also use ETFs, which are very similar to mutual funds, but trade a bit differently. My mutual funds are passive, index funds. There is no active management in these funds and they track an established index. This keeps fees low, and it’s not common for an actively traded fund to consistently outperform the index.

What am I hiding?

I’m not intentionally hiding anything, but I do have assets not listed above. I have 529 accounts for my boys. I’m a minor shareholder in a small craft brewery. We have our primary home and a modest cabin. These are real assets with value, but don’t figure into our retirement plans, so I choose not to include them in the spreadsheet I’ve shared with you. OK, full disclosure, the cabin and happy hour at the brewery may indeed factor into our retirement plans, but not in a way that affects the balance sheet.

Why so aggressive?

I’ve chosen a rather aggressive allocation. Increasing risk increases potential reward. I know from experience (that ugly 2008) that I’ve got the mental fortitude to watch my accounts lose half their value and not sweat it. Those accounts have bounced back nicely and I was buying on the way down and on the recovery upswing. My goal is to have 40 to 50 years of expenses saved up before actually retiring; this is considerably more than the 25 years’ worth often cited as required to be FI (financially independent) and RE (retire early).

There seem to be two schools of thought as to how to invest an oversized nest egg. Some would say, “You’ve won the game. Why keep playing?” Put that money in a very safe portfolio and you’ll never run out. You could go with a conservative portfolio of 80% bonds/fixed income and coast.

I say phooey to that. My plan is to allocate half of the nest egg (25 years of expenses) in a manner consistent with a typical retirement portfolio. With an extended retirement, that would probably be somewhere between 60/40 and 75/25 to maximize returns over the long haul with the larger stock portion while reducing volatility with the bonds.

With the other 15 to 25 years’ worth of expenses, I can be as aggressive as I want to be. I’m not saying that I’m putting half my portfolio into Malaysian microcaps. I just don’t have a good enough reason to play it safe with this half of the portfolio. It’s a cushion that I would love to see grow, but if it dropped in half it wouldn’t phase me or affect my long-term plans whatsoever. It’s also money that I may not touch for a very long time, if ever, and I’ll have time to allow it to recover.

Does this plan expose me to unnecessary risk? I suppose, although a diversified portfolio of index funds is light-years away from the riskiest way to invest a big pile of money. So why would I choose stocks over bonds for the overflow portion of my retirement portfolio? Because I can. Because I’m a man who likes to compete and win.

I’m willing to take the very slight risk that my accounts could shrink and never recover in order to reap the benefits of the much more likely outcome of continued growth that outpaces both bond returns and inflation.

I’m not interested in working until I’ve amassed an eight-figure portfolio, but I’d be lying if I told you I don’t like the idea of maybe having one someday. If it happens, I’d prefer to let the portfolio do the heavy lifting for me.