- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

Investment Fees Will Cost You Millions

A couple percentage points don't sound like much. But, over the course of a lifetime, those fees can subtract many millions from your investment portfolio.

Yes, millions.

You don’t have to be a big shot for this to be true. In fact, someone investing $833 a month into his 401(k) can see an 8-figure sum (that’s $10 million, people) disappear over the course of a long life span. Today, we will pry into the finances of four people you may encounter at the hospital and discover the net worth they might expect to have over the course of their working and retirement years.

What sort of annual investment fees are we talking about?

- Expense ratios of mutual funds (0.04% or less to 1.5% or more)

- Front-End Load or Back-End Load (Up to 5.75% is common)

- 12-b1 fees (marketing or distributing fee 0.25% to 1%)

- Assets Under Management Fees (0.5% to 1.5% of managed portfolio)

- Other (hourly rate, flat fee, admin fee, hidden fees)

None of these fees are mandatory, although the only way to avoid the first one is to completely avoid mutual funds and ETFs. The other 4 categories of fees can be avoided by staying away from fund companies that charge excessive fees and managing your own portfolio. I manage my portfolio made up almost entirely of Vanguard admiral funds, and the total annual fees are a shade under 0.1%.

To take a closer look at the effects of a range of fees on portfolio performance, I’d like to introduce my four friends. We’ll call them Agnes, Agatha, Jermaine, and Jack.

Jack, the nurse

Jack is a registered nurse. He likes his overnight shifts and early morning happy hours.

Jack has no desire to retire early. He enjoys life and invests enough into his 401(k) to receive the employer match, plus a little extra. At the end of each year, he’s got $10,000 invested, and he does this for 40 years from age 22 to age 62 when he retires.

To keep the calculations reasonably simple, we need to make some assumptions. In order to look at total dollars accumulated, we’ll use nominal (not adjusted for inflation) returns, assuming 8% during working years, and 5% returns with a lower-risk portfolio in retirement. In retirement, Jack will draw $60,000 a year from the portfolio to live and pay taxes. Both his investments during working years and withdrawals in retirement will be made at the beginning of each month.

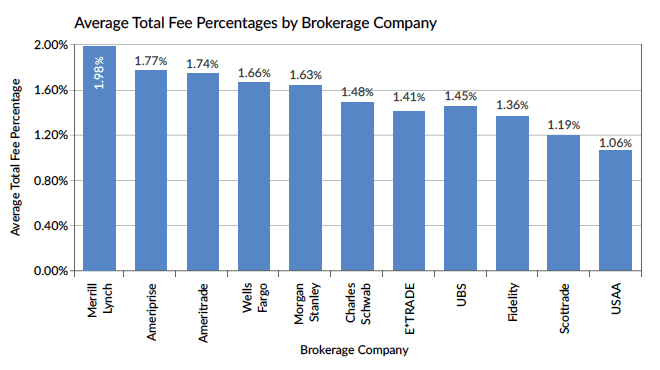

We’ll look at a realistic range of fees, from 0.1% to 3.0%. When working with reputable advisors, Personal Capital found a range of 1.06% to 1.98% in total average annual fees. Less reputable advisors could add another percent or so on top of that with loaded funds, frequent buying and selling within your account (a.k.a. churning) and hidden fees.

image credit Personal Capital

To Summarize our assumptions for Jack:

- $10,000 tax deferred annual investment, in monthly increments

- 8% nominal returns while working

- 5% nominal returns in retirement

- $60,000 withdrawn annually in retirement for spending & tax payments

- Fees could be as low as 0.1% and as high as 3%

- Jack works and invests from age 22 and retires at age 62

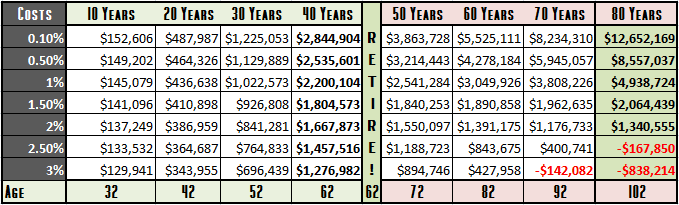

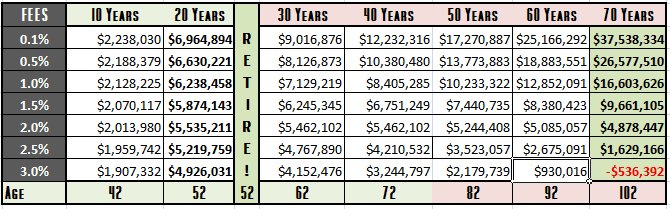

Jack’s 40 year career as a registered nurse

By investing $10,000 a year for 40 years, Jack can expect to amass anywhere from $1.28 million to $2.84 million, depending on fees. That’s a difference of $1.56 million dollars available at retirement. The DIY plan with 0.1% in fees grows to be 122% larger than the 3.0% fee plan.

And that’s not the half of it.

Continuing on into retirement, keeping spending constant at $60,000 a year, if Jack lives to be 100, he could have an 8-figure portfolio with the lowest fee structure. Or he could be out of money before his 90th birthday. If he survives to age 102, the difference between 0.1% fees and 3.0% fees exceeds $13 million!

If we were to account for inflation, Jack’s spending would likely increase progressively throughout retirement, although at some point, spending tends to decrease as the more adventurous travel days are behind him. Of course, long-term care could greatly increase his annual needs. Long story short, we don’t know what to expect, but in the most realistic scenario, due to inflation, Jack would be more likely to run out of money even earlier in the scenarios with high fees.

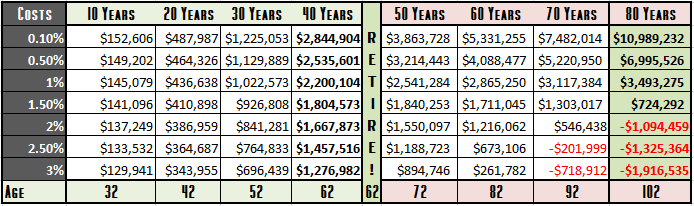

Here’s a look at Jack’s balances if he increased spending by 25% in each of the first 2 decades of retirement and then held steady

Jack’s spending in this scenario will be:

- $60,000 from age 62 to 72

- $75,000 from age 72 to 82

- $93,750 from age 82 to 102

Well, the numbers have changed, and it doesn’t look any better for the high fee scenario in this somewhat more realistic version. The difference between the savvy DIY investor and the investor with high fees is still about $13 million if he gets to be a centenarian.

Fees (and fawns) can come back to bite you.

Agatha, the psychiatrist

Agatha is a psychiatrist employed by the hospital. She enjoys plush leather chairs and just listening.

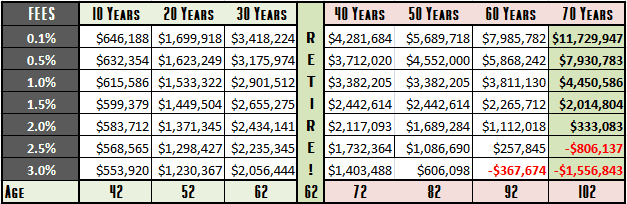

Getting a later start, Agatha will have a shorter career than Jack, but retire at the same age of 62.For 30 years, Agatha will be investing $50,000 a year into tax deferred retirement plans.

She will receive the same investment returns as Jack, 8% while working and 5% in retirement. Her retirement spending will be a loftier $100,000 annually.

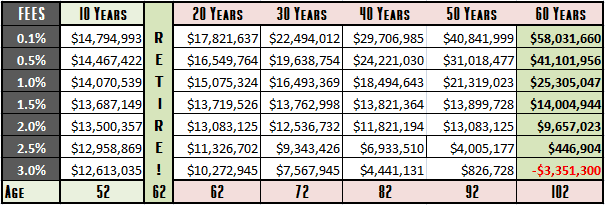

Agatha’s 30 year career as a psychiatrist

Agatha builds up a larger nest egg than Jack, but by virtue of larger retirement spending, she is at a greater risk of depleting it. Again we see the ginormous disparity between fees of 0.1% and fees of 3.0%. Again, the difference exceeds $13 million if Agatha gets off the couch and does some cardio, giving her a fighting chance to live to 102.

Jermaine, the surgeon

Jermaine is an orthopedic surgeon in an independent group. He enjoys “bone broke” & “me fix”. That’s a BBMF for those keeping score at home. [I kid, I kid…]

Jermaine, who had to be one of the top students in his medical school class to land a spot in ortho, is quite savvy with his finances. He works hard, but doesn’t want to do so forever. Like the PoF, Jermaine has FIRE plans of his own, and plans to work a twenty-year career, retiring at 52.

For 20 years, he invests $150,000 a year, with $50,000 tax deferred and $100,000 in a taxable account. In this scenario, his taxable investments will experience tax drag.

Assuming a buy-and-hold portfolio with a 2% annual qualified dividend (similar to Vanguard’s Total Stock Market or S&P 500 index funds) and a 30% total tax on qualified dividends, his taxable account sees a tax drag of 0.6%, so the overall portfolio will experience a tax drag of 0.4%. (We’ll ignore the small amount of drift the portfolio would see as the tax deferred portion grows at a slightly quicker clip.)

Compared to our first two friends, the investment returns will be the same (8% and 5%) but we’ll subtract 0.4% from those before subtracting fees in our calculations. Retirement spending will match his earlier savings amount, $150,000 a year.

Jermaine’s 20 year career as an orthopedic surgeon

Twenty years of solid investments make Jermaine a wealthy individual. $5 million to $7 million at age 52 depending on fees. What happens in retirement? If the good doctor eats well and exercises like he did as a standout collegiate gymnast, he too might make it to 102. At this point, he might have $37 million or be flat broke. It depends entirely on the investment fees.

“he might have $37 million or be flat broke. It depends entirely on the investment fees.”

Agnes, the executive

Agnes is the CEO of a large multi-state health system. She worked her way up the ranks and bounced from one time zone to another for decades to find herself in this enviable position. Hermonthly salary dwarfs her friend Agatha’s annual salary. Agnes enjoys endless meetings and flushing caviar down the toilet just because.

Agnes becomes the CEO at age 52, and invests a cool $1 million per year, $50,000 into a tax deferred account and the remaining $950,000 into a taxable account. With only 5% tax deferred, we will factor in a 0.55% tax drag on the account. She will retire in 10 years at age 62, spend a lofty $400,000 in a luxurious retirement, and the assumptions on investment returns remain the same.

Agnes’ 10 year career as as the CEO

The brief accumulation phase is good to Agnes. She will have $12.6 million to $14.8 million depending on fees. If those fees persist into retirement, we see the gap widen tremendously, to $15 million at age 72, $25 miilion at age 82, $40 million at age 92, and better than $60 million at age 102, at which poor Agnes with the 3.0% fees finds herself several million dollars in debt, while the ultrarich Agnes with 0.1% fees has enough money to name her alma mater’s new football stadium after her favorite cat.

I had my own “Where are the Customers’ Yachts?” moment early in my anesthesia career. A friend who was working in the finance industry (I can’t tell you with which company; it would violate my Principals) invited me to join him and his mentor and a few close friends for a tailgate and college football game.

My friend’s mentor had ten of the best seats in the stadium and a few tailgate spots that cost a few thousand each for the season. If I was supposed to be impressed, I wasn’t. All of this was being paid for with other peoples’ money in a zero sum investment game. At the end of the day, I understood just how important it was to learn to manage my own portfolio. My investment gains could easily become somebody else’s luxury box. No thank you.

Learning how to invest pays, and that’s a fact. Just ask my friends Agnes, Agatha, Jermaine, and Jack. If you already know what you need to know to manage your own portfolio, strong work!

If not, the sooner you get started, the sooner you will find yourself on the path to real wealth and freedom.

Would you like to enter your own data into a spreadsheet like you see above? Check out the customizable Fees Effect Calculator on the Calculators page at PhysicianOnFIRE.com.

Do you know what you pay in fees? What fees do you see as justifiable? Would you rather end up with an 8-figure portfolio or be flat broke? It’s a silly question, but many people make choices that are more likely to make them the latter.