- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

Cost Basis Methods Can Help Save You Taxes

There are a number of cost basis reporting methods and some will save you more money in taxes than others.

In my last article, I discussed the new IRS rules for reporting the cost basis of your investment purchases in a taxable investment account. Recall that the cost basis is the net investment you make into a particular stock or mutual fund.

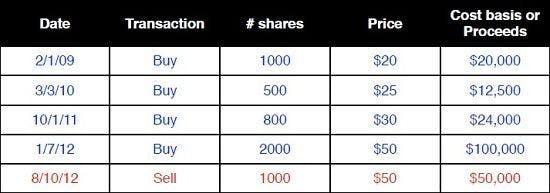

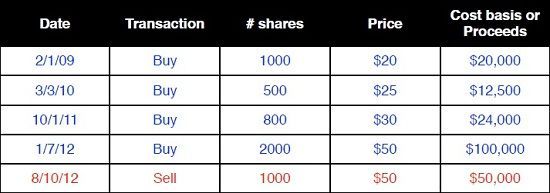

Suppose you make the following transactions in a mutual fund over the past few years:

What gain do you have to report on Schedule D of your income tax return?

That depends on what method of cost basis reporting you’re going to do. There are more cost basis reporting methods now then there were a few years ago. While I don’t have the space to cover all of them, let’s take a look at two of them to see how you can save a ton of money and reduce your tax bill.

One method is the First In, First Out (FIFO) method. With FIFO, the shares sold are automatically matched to the earliest shares you bought. So the sale of 1,000 shares on 8/10/12 would be matched with the buy shares on 2/1/09. This means your total gain is $30,000 ($50,000 in proceeds minus 1,000 x $20 in cost basis). With the capital gains tax at 15% and assuming a state income tax of 5%, you’d owe about $6,000 in taxes on the sale.

But there’s another cost basis reporting method you can use — called Highest In, First Out (HIFO). In this method the sale of shares is matched to the shares bought for the highest share price. So the sale of 1,000 shares on 8/10/12 would be matched with the buy shares on 1/7/12, resulting in a gain of $0 and a tax liability of $0. In this example, using the HIFO method saved you $6,000 in taxes. Don’t ignore the minutiae

To make matters worse there are other factors that come into play here. If you’ve been reinvesting dividends, each dividend reinvestment adds another cost basis lot to the pool. If you’ve been in an investment for many years and have been reinvesting dividends all along, you could potentially have dozens of cost basis lots to keep track of.

Anytime you sell partial shares, you then need to readjust your cost basis in the remaining shares that you matched up the sale with.

If you sell shares for a loss, you need to figure out which cost basis lot you want to use.

Finally, for gains, the tax rates for short-term gains (gains on shares held less than one year) are higher than long term gains. So it’s possible that you could pay more tax by selling short-term shares for a lower gain than by selling long-term shares that have a higher gain.

Are we having fun yet?

What you need to do

Unfortunately many CPAs simply report the proceeds from the sale and then expect you to tell them what you bought these investments for and the cost basis. A good fee-only investment advisor should do this for you, but most simply don’t take the time to figure out how you can reduce your tax bill by using the right cost basis methods, readjusting cost basis after the sale and considering long- or short-term gains.

So here’s what I suggest you do:

1. Create a spreadsheet detailing all buy and sell transactions and calculating net cost basis for each of those lots. Do this for all investments in your taxable accounts.

2. Change the cost basis reporting method you use with the custodian who holds your account. HIFO is generally better, but there are others that may be more beneficial to you.

3. Breakdown your cost basis lots into non-covered and covered shares

4. Before you sell, think about which cost basis lot may result in your lowest tax liability, taking into consideration short-term versus long-term gains. Then readjust your cost basis for the original shares you bought if you sold only part of the original lot.