- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

Disability Insurance for Physicians: Does Your Coverage Measure Up?

Long-term disability coverage is important for many occupations, but for physicians it’s particularly critical. Even a relatively minor accident or illness can interfere with their ability to practice medicine.

Long-term disability coverage is important for many occupations, but for physicians it’s particularly critical. Even a relatively minor accident or illness can interfere with their ability to practice medicine. And for many physicians — especially younger ones — future earnings potential is their biggest asset.

Disability insurance is designed to protect this asset by replacing your income in the event a disability prevents you from working for an extended period of time. Unfortunately, many standard disability policies fall far short of this goal. To ensure that you and your family are protected, you should evaluate your current coverage and consider purchasing additional insurance to close any gaps.

What’s Your Disability Gap?

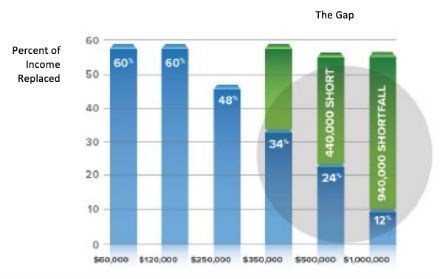

The first step is to measure the gap between your current income and the benefits your disability policy provides. A basic individual disability policy typically covers 60 to 65 percent of your current monthly income when you start practicing, but these policies also place a cap on monthly benefits — usually the most you can obtain is between $5,000 and $15,000 per month. As your income grows, your disability may not be able to continue to insure all of your after-tax income. Thus, you will have a gap in protection and exposure.

How Traditional Group LTD Plans Discriminate Against the Highly Compensated

Example shown: Group LTD covers 60% of earnings up to $10,000 per month.

It’s also important to consider taxes. Generally, benefits received under an employer-paid plan are taxable, but if you pay the premiums using after-tax dollars, the benefits are tax-free. A 65-percent tax-free benefit would likely come close to duplicating your after tax income (assuming the monthly limit is high enough).

High-end disability programs can fill the income gaps left by standard policies. As you weigh your coverage options, here are the most important policy provisions to consider:

Coverage amount. Look for a policy with a monthly benefit that’s sufficient to comfortably meet your monthly budget in the event an extended disability causes your income to take a hit. The best policies offer maximum benefits of $50,000 to $100,000 per month or more and cover up to 75% of your current income.

Guaranteed Issue. High-end group disability programs may offer guaranteed issue policies, which cover participants without the need for a medical exam. This is a huge benefit for groups whose members have pre-existing conditions.

Definition of total disability. The most comprehensive policies provide benefits if you’re unable to perform the “material and substantial” duties of your “own occupation.” Policies that provide true own occupation coverage pay full benefits even if you get work in another occupation and regardless of how much you earn. For example, a surgeon who injures her hand would be eligible for benefits even if she gets a teaching job at a medical school. Some policies define “own occupation” as your specific medical specialty. So, for example, a physician who is unable to perform surgery would receive benefits even if he is able to practice internal medicine.

Some policies contain “modified own occupation” provisions. They provide coverage if you’re unable to perform your regular occupation, but reduce or eliminate benefits if you find gainful employment in any occupation. Others contain “transitional own occupation” provisions, which scale back benefits once your combined benefits and earnings from other occupations exceed your pre-disability income.

The least generous policies consider you to be totally disabled only if you’re unable to perform the material and substantial duties of any occupation.

Residual or partial disability. Residual or partial disability benefits are critical. After all, even something less than total disability can have a significant impact on your earnings. These benefits vary widely among policies, so it’s important to examine these provisions carefully. Typically, benefits are triggered when an illness or injury causes your income to drop by a specified percentage. Twenty percent is standard, but some policies offer a 15 percent income-loss threshold.

Most of these policies pay a 50 percent benefit for the first six months to one year of a partial disability claim, although some base benefits on your actual losses. Most also pay 100 percent of your monthly benefit once your income loss reaches 75 or 80 percent of your pre-disability earnings.

Recovery or transition benefits. These provisions recognize that even after you recover from a disability, the impact on your earnings persists as you strive to rebuild your patient base. Some policies offer recovery benefits for a limited period of time — such as 12 or 24 months — while others pay these benefits for the duration of the benefit period.

Benefit period. The maximum length of time benefits will be paid varies widely among disability policies. Some policies pay benefits for as little as two years, while others continue benefits to age 65 or longer. High-end supplemental policies, particularly those that offer guaranteed issue, typically have shorter benefit periods (five years is common). But riders are available that provide large lump-sum payments at the end of the benefit period. The best policies are noncancelable (meaning premiums won’t increase) and guaranteed renewable throughout the benefit period.

Future increases. It’s important that your disability benefits keep pace with inflation and future increases in your income. Look for a policy that offers cost-of-living adjustments and the option to purchase additional coverage without the need for a medical exam.

Elimination period. An elimination period is essentially a deductible. It’s the amount of time — typically 90 days — that you must bear the cost of a disability before benefits kick in. One critical consideration is whether the policy requires 90 consecutive days of disability or 90 total days of disability over a specified period (such as 180 days). If it’s the former, the 90-day period will start over each time you return to work, no matter how brief.

Other benefits. Many policies supplement monthly benefits with lump sum benefits for permanent disabilities. These benefits can be used to fund a buy-sell agreement, replace retirement plan contributions or purchase long-term-care coverage. Some policies can be converted into long-term-care policies at retirement age.

Not all disability policies are created equal. Don’t assume that you and your family are protected against financial loss just because you’re covered by a standard group or individual disability policy. Scrutinize the policy’s terms and consider acquiring supplemental coverage if your current program fails to provide the financial security you desire.

####

Securities offered through Niagara International Capital Limited (Member FINRA/SIPC). Schechter Wealth and Niagara International Capital Limited are not affiliated. Check the background of Niagara International Capital Limited and its registered representatives at FINRA’s BrokerCheck. Securities are only offered and broker-dealer transactions only occur at the registered Niagara branch location of Birmingham, MI.

About Schechter Wealth

Schechter Wealth is a boutique, third generation wealth advisory firm. For over 75 years, our multi-disciplined team consisting of one or more JDs, CPAs, LLMs, CLTCs, CLUs, PFSs, CAPs, MBAs, CIMA participants®, CFP® practitioners and CFA® charterholders has been quietly advising wealthy families on financial matters including institutional quality investment advisory services, advanced life insurance planning, income and estate taxes, business succession and charitable planning. www.SchechterWealth.com

Jason Zimmerman, MBA, CLU, CAP

Managing Director

As one of the Senior Managing Directors and owners of Schechter Wealth, Jason Zimmerman is responsible for helping to define the strategic direction of the firm. Schechter is primarily focused in the areas of Life Insurance based planning solutions, Investment alternatives, and Employee Benefits. He also manages relationships with referring and strategic partners such as insurance professionals, banks, CPA’s and money managers to help further grow our advanced life insurance planning area. In addition, Jason works directly with the firm’s clients and their advisors in the execution of sophisticated solutions in wealth accumulation and preservation, wealth transfer and charitable giving.

Jason has earned designations that help clients with financial planning, income taxation, retirement planning, investments and estate planning. The designations are: The Chartered Life Underwriter (CLU) designation for professionals involved in the areas of estate planning and business succession planning; and the Chartered Advisor in Philanthropy (CAP) designation.