- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

How a Sabbatical Affects Your Finances

The timing of a sabbatical can alter the long-term financial impact of the time off. Taking a year off before launching a career may be the best option.

The last time we revisited Dr. Carlson, we explored theimpact of a higher salaryand learned that a 33% raise shortened her time to FI by a similar percentage.

<p style="margin: 0.75em 0px; padding: 0px; border: 0px; font-style: normal; font-variant-ligatures: normal; font-variant-caps: normal; font-variant-numeric: inherit; font-weight: normal; font-stretch: inherit; font-size: 17.6px; line-height: inherit; font-family: Lato, Arial, Tahoma; vertical-align: baseline; color: rgb(17, 17, 17); letter-spacing: normal; orphans: 2; text-align: start; text-indent: 0px; text-transform: none; white-space: normal; widows: 2; word-spacing: 0px;

Today, we’ll investigate the ramifications of a completely different scenario: taking a break.

As we have done in our other revisits to our4 physicians, we will alter their fate at a point 11 years after we were first introduced to them, the point where Dr. A became financially independent.

So Dr. Carlson has been making a good living, working hard, and starting to feel that 11-year itch. Symptoms ofburnout are beginning to manifest. She is struggling to find joy in the day-to-day grind. Dr. C decides to take an extended timeout from her career.

After some discussion, Dr. C is able to negotiate a one-year absencefrom her job. For 12 months, she will have no earned income. Intelligently, Dr. C plans to take her sabbatical from July to June in order to earn a half year’s income in each of two calendar years. By doing so, she will be able to continue contributing to tax deferred retirement accounts, while paying a much lower tax bill in two consecutive years.

To keep things interesting, we can compare the outcome with a choice to take a full calendar year off from January to December. An additional comparison can be made by having Dr. C start her career one year later, showing us the cost of deferring for one year prior to beginning medical school, or needing an additional year to gain acceptance.

I can’t tell you how Dr. Carlson plans to spend her year off. I can think of a whole lot of fun and relaxing ways to spend that time, but I’m not Dr. C. Maybe she sails around the world, from oneIsland In The Sun to another. Perhaps she never leaves the county, and volunteers at the local free clinic to keep up her skills. Hopefully, she will take advantage of the sabbatical to find time for personal growth, travel, sleeping in, and connecting with family and friends.

![On a [Galapagos] Island in the Sun](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2F0vv8moc6%2Fmedec%2F6aaae737667a4e2a75d7559c3f23e2c0525ddb57-450x450.jpg%3Ffit%3Dcrop%26auto%3Dformat&w=1080&q=75 "On a [Galapagos] Island in the Sun")

On a [Galapagos] Island in the Sun

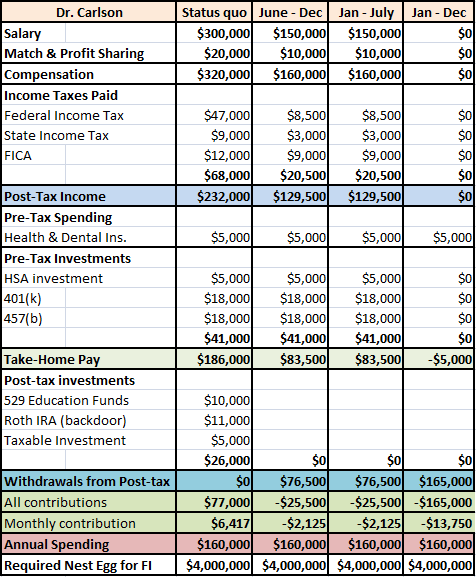

I do know that Dr. C has some fixed expenses and she’ll find ways to spend money with her newfound free time. To keep the calculations simple, we’re going to assume that her family’s expenses remain the same throughout her year off. That is, the budget will remain steady at $160,000 a year in our calculations.

In the July to June year off, Dr. C has taxable income every year and is able to contribute to tax deferred retirement plans. To cover her costs though, she must sell some from her post-tax accounts each year to make up for a $74,500 shortage. I say post-tax accounts, rather than taxable account, because the taxable account won’t be quite enough to cover the $149,000 she needs. Thankfully, Roth contributions (but not earnings) can be withdrawn tax-free and penalty-free.

In the January to December calendar year off, she is unable to invest any money with no taxable income (although her already sizable investments will continue to grow). To cover her spending and health insurance, she’ll have to come up with $165,000 from her post-tax accounts.

Is $5000 realistic for health insurance for a family of four? Probably not, but I’m keeping the number consistent, assuming she has a HDHP with HSA, and being a few thousand off means little when we’re looking at spending of $160,000 a year and a nest egg in the millions. If health insurance costs her $15,000, she should be able to trim $10,000 from her fat $160,000 budget to cover it.

Here’s a look at what these years might look like for Dr. C.

It’s incredible to see how much taxes decrease with a lower salary, as we saw when looking atDr. A going part-time. Of course, taxes are even lower when you have zero salary coming in, a situation exists when taking a January to December calendar year off.

There would be some long-term capital gains realized when selling off the taxable account, but not enough to push her out of the 15% tax bracket, so she won’t pay any taxes on those gains (or qualified dividends), a fact emphasized in one of my favorite posts,The Taxman Leaveth.

How will the year off affect her nest egg in the coming years? The following table shows us its size at our starting point, 11 years into her career (or 10 with the one-year delayed start), at 13 years (after the sabbatical), 20 years, and finally when realizing FI after a 28 to 30-year career.

As we know from the original4 physicians, maintaining the status quo will allow Dr. C achieve her FI goal of $4 million after about 28 years, most likely approaching age 60.

Timing matters.

Taking the June to Julysabbatical makes her $214,000 less wealthy at the 13-year mark (shortly after completing the sabbatical), and $283,000 less wealthy at the 20-year mark. Her FI target of $4 million is achieved a few months shy of a 29-year career. In other words, the 12 months off delayed her potential to retire with the same nest egg by about 20 months.

The Janueary to Decembersabbatical costs her a bit more, because she is unable to spread her income out over two calendar years and take advantage of lower tax brackets in those years. She is also unable to make any tax-deferred retirement contributions or receive a match in her year off. That difference ends up being $73,000 after 29 years, adding about 3.5 months to her time to FI when compared to the June to July sabbatical. In this scenario, the 12-month sabbatical extended her time to FI by 23.5 months.

one-year deferral?

What about theShouldn’t that have the most damaging effect, since the lost wages would rob her of so many years ofcompounding? It wouldifwe assumed that she had a $160,000 spending habit and earned nothing during that deferral year. Of course, most new college grads are not spending like a doctor who brings home $300,000. Most likely, she was still living like a college student, and finding a way to make ends meet while enjoying her year off.

For the sake of this comparison, I’m assuming her year off in her early twenties was a break-even year. No savings, no debt, just a year of coasting, most likely with at least a part-time job. Therefore, FI is delayed by exactly a year, and she will always be one year behind where she would have been if she had not taken a extra year before starting down the path towards being a physician.

In essence, future Dr. C borrowed one year from retirement and used it early in life. During deferral, she has youth and health on her side, but very little money. Foregoing deferral, she will be able to retire a year earlier, but won’t have youth, and may not have the health she enjoyed in her twenties. She will have plenty of money, though!