- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

Physician vs. Financial Advisor Income: What Lessons Can Doctors Learn?

Physicians face a seemingly difficult choice of whether to self-manage their expendable income, or whether to hire a financial advisor. A look at the median incomes of physicians and advisors provides some insight.

Early in my financial career, I was on the board of a group of financial professionals in Indianapolis. The idea was to serve my community and have the opportunity to create relationships with others in the same field. During one of our meetings we were asked to introduce ourselves. I said something to the effect that I had been a practicing neurologist but retrained and now was working in the financial industry. The person next to me said (admittedly to be funny) that he was a financial professional but now planned to retrain to become a doctor. Everyone laughed. It was absurd that he would do such a thing. Becoming a so-called “financial professional” can take as little time as a few months. Becoming a physician is a commitment of at least 6 years.

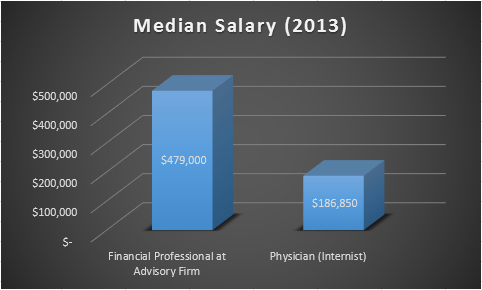

This contrast between the 2 training period makes what I am about to say even more difficult to comprehend. It is a statistic that is just as ridiculous as the statement of my colleague at our board meeting. In 2013, the median income of financial professionals at an advisory firm was $479,000. For an internist, it was $186,850. The difference is $292,150 in favor of the financial professional. To be clear, I am not talking about the so-called financial professionals at brokerage firms that act as brokers by taking client orders, etc. but those at advisory firms that offer advice. Brokers make less, by some estimates around $99,000.

The financial professional at an advisory firm may be a Certified Financial Planner (CFP) or a financial advisor. The training for a CFP is 2 years. To become a financial advisor it is far less. Normally, it is necessary to pass 2 investment tests, the so-called 7 and 63. A 63 securities license entitles the holder to solicit orders for any type of security in a particular state (definition from Investopedia). A 7 entitles the holder to sell all types of securities products with the exception of commodities and futures (definition from Investopedia).

Wells Fargo estimates that it takes about 10 weeks of study to pass the 63 and 7. Then there is further in-house training. For example, at Schwab, my formal program was about 3 months with on-the-job training as well. Although I no longer remember the sequence of the last 2 firms I worked at, one of the 2 was a boutique advisory firm and at each I was called a financial advisor.

Contrast this training to an internist. Normally, she will have attended medical school for 4 years and then rotated through 3 years of specialty training after that, a total of 7 years. Whereas a financial professional may have had as little as several months of education.

Who pays the advisors at advisory firms a median of $479,000 per year?

Their CEOs, of course, make that decision. But the money comes from the firm’s clients, many of whom are physicians.

Is this a good use of the clients’ money? Are they receiving bang for their buck?

This would be a good investment for a doctor if her advisory firm portfolio did better than the market. Statistics, of course, do not bear this out. So, for doctors, or anyone who wants to put more money in her pocketbook, managing her own expendable dollars is ideal. There are those, however, who simply are not interested or able in self-managing, and then professional management is a better choice. But, if you are in the “take charge” group and willing to learn, here are some options to help begin the journey: