- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

Saving Money on Investment Advice: Robo-Advisors

As the name suggests, Robo-advisors are not going to provide warm and fuzzy service like the human advisors to which investors are accustomed. But, Robos are less expensive, which brings up this question, "Can investors give up the good feelings a mortal imparts in exchange for paying less?"

Jack, Jill and Joe have $1 million investment portfolios. Each receives advice from specialists. Jack pays $10,000 a year; Jill, $840.00 and Joe, $1,500.00. What’s going on here?

Photo from RoboCop, a remake of the 1987 movie, starring

Joel Kinnaman and Gary Oldman. Courtesy of Sony Pictures.

As the name suggests, Robo-advisors are not going to provide warm and fuzzy service like the human advisors to which investors are accustomed. But, Robos are less expensive, which brings up this question, “Can investors give up the good feelings a mortal imparts in exchange for paying less?”

Looking at the numbers, the answer is yes, for some. Wealthfront, one of the Robos, advertises that it manages over $1 billion in assets. Others in this same group include Betterment and FutureAdvisor. They all take over control of the client’s portfolio and manage it under their own umbrella. Each offers a diversified passive approach that is normally monitored frequently for rebalancing and tax-loss harvesting. The charge is 15-35 basis points or 0.0015% to 0.0035%. This is a bargain when personal advisors collect around one percent (0.01%) of assets under management.

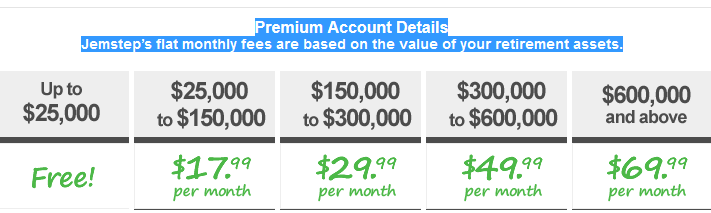

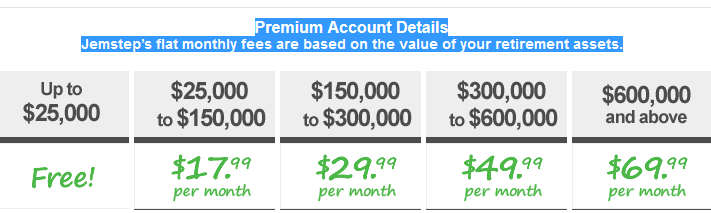

Another group of Robos, Jemstep and SigFig, basically do what Wealthfront, Betterment and FutureAdvisor accomplish without managing assets directly. Instead, the client makes any portfolio changes herself based on optimizers the company’s software models offer. The cost for this service is less because the client does part of the work. Jemstep, for example, charges on a progressive scale according to the client’s assets but tops out at $600,000 (see below). Smaller portfolios up to $25,000 are free. Thus, at Jemstep, the fee is basically 0.001% for portfolios $600,000 and above ($839.88/$600,000). This cost, $839.88 per year compared to $1,500 (0.0025%) for Wealthfront or roughly $6,000 (0.01%) for a personal advisor, is a bargain. Over time, this cost savings can make a monumental leap in the monies available to a retiree. This is because more money is invested rather than siphoned off by an advisor every year.

Jemstep advertisement

Robos use specialized computer programs to provide financial solutions for their clients. In other words, the human element is largely removed. Some would say this is good. Others would argue the opposite.

Whatever the case, I expect Robos are here to stay. When people can make money by saving it, they frequently choose that option. That is, unless she is too tethered to a human advisor that makes her feel good, often at an expense many people cannot afford.

For More:

What is Your Advisor Charging You?

Your Advisor's Compensation Has Increased Dramatically

Taking Control of Your Finances

Contain Expenses to Increase Returns

This information and content is offered for informative and educational purposes only. MyMoneyMD, LLC is not acting as a Registered Investment Advisor, Investment Counsel, Tax Advisor, or Legal Advisor.