- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

Specialty Choice and Financial Indpendence: Salary Matters

The choice of medical specialty shouldn't be made solely on income, but it cannot be ignored that salary will have a substantial impact on wealth creation.

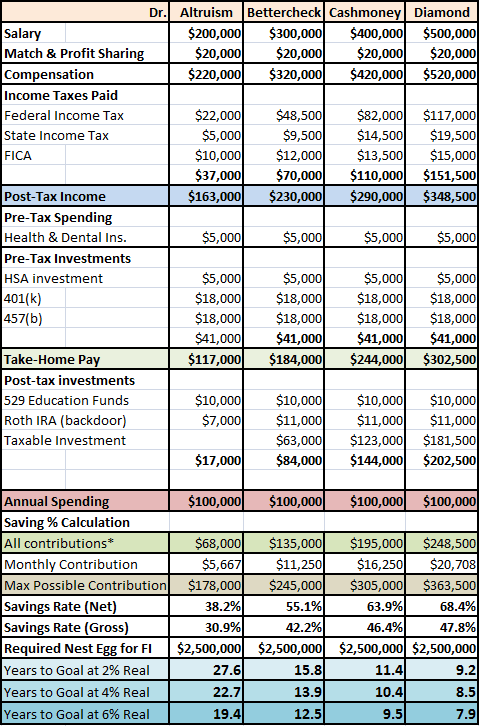

In each of our previous looks at the4 physicians, each doctor had a baseline salary of $300,000. We looked at the impact ofmaking more money with a job change, and making less byworking part-time.

However, we haven’t yet discussed the impact of a range of salaries on the ability to achieve financial independence. For this exercise, we will be dismissing Drs. Anderson, Benson, Carlson, and Dahlgren for a new set of characters, Drs. Altruism, Bettercheck, Cashmoney, and Diamond.

Dr. Altruism makes $200,000 a year.What specialties make about $200,000 a year? According to a recent survey, doctors in the following specialties have average salaries of $204,000 to $241,000.

- Pediatrics

- Endocrinology

- Family medicine

- Infectious disease

- Allergies

- Internal medicine

- Psychiatry

- Rheumatology

- Neurology

Dr. Bettercheck earns a better check, equal to $300,000for our analysis, by working in one of the following specialties, with a range from $266,000 to $329,000.

- Pathology

- Nephrology

- Ob/Gyn

- Pulmonary

- Critical Care

- Ophthalmology

- Emergency Medicine

- General Surgery

- Oncology

Dr. Cashmoney went into a high-paying specialty, earning $400,000 a year.The following physicians are pulling in from $355,000 to $443,000.

- Anesthesiology

- Urology

- Radiology

- Gastroenterology

- Dermatology

- Cardiology

- Orthopedics

Dr. Diamond Is crushing it in the dollar department, earning $500,000 per year.This physician is most likely in private practice in a high-paying specialty, and may be supplementing income withlocum tenens work. He or she may be an entrepreneur, with an ownership stake in a surgery center, imaging center,brewery, or billing company. It is not unheard of for a busy medical professional with a lucrative practice to earn seven figures. For our calculations though, we’ll examine the effect of a half-million dollar salary.

Just as we have done in the other4 Physician posts, we make the following assumptions when crunching numbers: the physician is married, in a one-income household with two children at home. They start this exercise with a net worth of zero, perhaps a few years removed from training.

Each physician will have an annual budget of $100,000. This is enough to live pretty well in most parts of the country. In Manhattan orSan Francisco, and some other high-cost-of-living areas, it would be more challenging. In rural areas, these physician families could live like kings and queens.

Not Dr. D’s home

Note that the budget will not rise with rising salaries. Although such a trend is typical in real life, the amount of money required to live a fulfilling and happy life doesn’t increase along with salary. If you can’t possibly be happy with $100,000 after-tax dollars to spend each year, your problem is probably not a lack ofmoney, but something else.

To reiterate, required annual spending is related to annual salary in the following ways:

- absolutely

- none

With that out of the way, let’s look at a hypothetical breakdown of our four physician’s salaries, including where the money goes, and how long it will take each of them to accumulate 25x annual spending, or $2.5 million, to be considered financially independent.

Each of our physicians would be considered an excellent saver, by virtue of their 31% to 48% net (38% to 68% gross) savings rates. How do they save so much? By spending “only” $100,000 a year. Calculate your own savings ratehere.

Comparing Dr. A with Dr. D, you can see that Dr. D pays over four times the taxes, despite making two-and-a-half times the income. But, by keeping spending equal, Dr. D is able to invest nearly four times as much money towards retirement. This results in financial independence in eight or nine years, whereas Dr. A will be working for 19 to 28 years, assuming reasonable returns of 2% to 6% real.

Do physicians in higher-paying specialties typically reach FI sooner than their counterparts in primary care? I don’t have any hard data, but anecdotal evidence suggests that the answer is “no". In reality, spending can easily rise in step with increased income, sometimes eclipsing it, leading to a scenario in whicha doctor can never retire with the usual definition offinancial independence. Of course, it doesn’t have to be this way, and many of my readers are mold-breakers. Physician devotees of theBogleheads,WhiteCoatInvestor, orMr. Money Mustache may be doing as well or better as our fictional Dr. Diamond.

Money isn't everything.

While it’s clear that a $200,000 salary will prolong the path to financial independence, the goal is not out of reach, and should be achievable for most physicians in their fifties.

Sliding up the pay scale, Dr. B needs an extra four to six years to achieve financial independence, and Dr. C needs only a couple additional years as compared to Dr. D. It’s better to spend fifteen years working in a job you enjoy compared to eight or nine in a stressful job that mightburn you out. Specialty choice, or job choice, should not be made based on salary alone.

How should you choose a specialty?

The answer is beyond the scope of this personal finance blog, but I’ve found a few fun flowcharts that may be usefulhere,here, andhere.

Personally, I’m a Dr. C, having chosen a specialty that pays pretty well, and is compatible with my personality and work ethic. I would never recommend choosing a specialty solely on the income potential, but it is a factor worth considering, particularly if you are on the fence between two specialties you might find equally rewarding in all other aspects.

Physicians, are you happy with the specialty you chose? What specialty or specialties would you recommend to someone starting medical school today?