- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

The Impressive Financial Impact of Working After Financial Independence

What happens when a physician obtains financial independence, and chooses to continue working another 5, 10 or 20 years? Incredible wealth is attainable.

In the first Tale of 4 Physicians, we analyzed the impact of different spending budgets on wealth creation.Each of our 4 physicians was married with 2 kids and had a household income of $300,000.

I’d like to revisit one of these physicians, crunch some more numbers, and learn what might happen to her nest egg if she were to continue working by choice after achieving financial independence (FI).

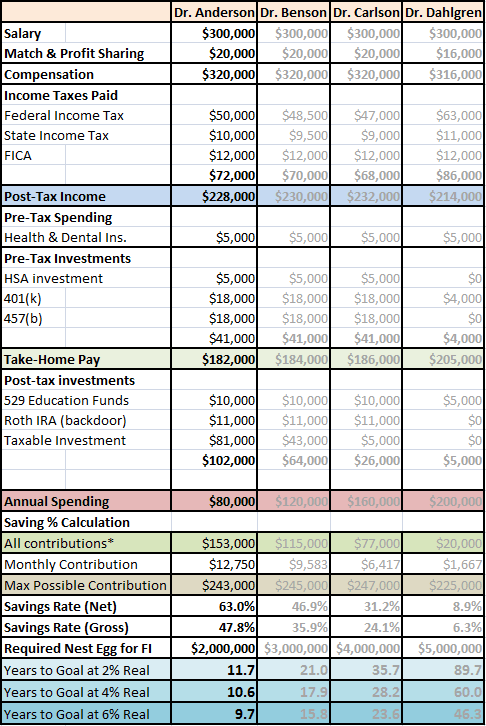

Dr. Anderson was the most frugal of our 4 physicians.Dr. A had household spending of $80,000 a year.She had a net savings rate of 64% and was on track to be FI in about 10 years, give or take a year.Let’s have another look at her numbers.

OK, fast forward 11 years.Dr. Anderson has stayed the course, her index funds have given her market returns, which haven’t been stellar, but have outpaced inflation by 4%.She’s got a nest egg with the purchasing power of about $2 million in today’s dollars (she’s got closer to $2.5 million but inflation has eroded the purchasing power*).She doesn’t love every aspect of her workday, but finds fulfillment in providing care to her patients.She knows that she could retire today, and likely have enough money to support her and her family indefinitely with a 4% withdrawal rate.

But there are many uncertainties.She won’t be eligible for medicare for more than 20 years and she has no idea how our health care system might change in the meantime.She and her husband may live another 50 years or more.

From her reading, she knows that the 4% withdrawal rate was considered safe for a 30-year retirement.She recently read an article that convinced her that 3% might be safer.She can’t imagine retiring in her early forties after all the sacrifices she has made to practice medicine, which she still feels is her calling.She is not ready to hang up the stethoscope and she wonders how her financial picture might change if she chooses to work another 5 or 10 years.

T

Allow me to channel my inner mathlete and work some numbers for Dr. A.To keep things simple, we’ll use real (inflation adjusted) return, rather than nominal return.hat will keep us looking at dollar amounts in terms of their purchasing power today.

We’ll also assume that she’ll maintain a budget equal to $80,000, even after the mortgage is paid off and the 529s are fully funded.Perhaps she’ll use that money to travel more or for charitable causes.

We’ll look at her future nest egg balance if she were to retire now, in 5 years, in 10 years, and in 20 years with 0%, 2%, 4%, and 6% real return rates.

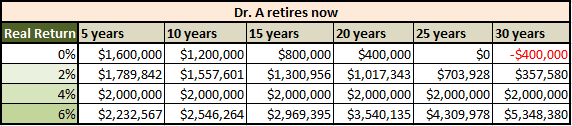

What if Dr. A retires now?

If Dr. A retires now and maintains her current level of spending, the equivalent of $80,000 today, she’s got a good shot at making her money last.If she earns 4% real, her nest egg will remain steady.A better return will allow her nest egg to slowly grow while she lives out a long, comfortable retirement.If her baseline spending exceeds her returns, she will watch that nestegg shrink over time.If it only keeps up with inflation, a 0% real return, she will run out of money in 25 years.Doh!

Can Dr. A avoid catastrophe in the case of a long-term sluggish market?Sure.She should expect have a social security check coming her way eventually, having contributed the max for 11 years.She’ll be able to cut back on expenses in lean years, more easily after the mortgage debt is gone.What are the odds of 25 years of 0% real return?If she has a diversified portfolio, I would say it’s quite slim.Even the best case scenario offered, a 6% real return, is below what the stock market has given in the modern era.

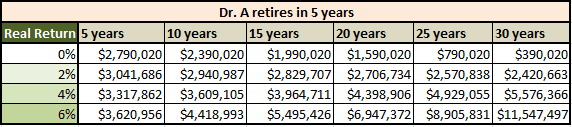

How do the numbers change if Dr. A decides to continue working and retire in 5 years?

Dang!Even in the worst given scenario, she’s doing alright.The odds of running out of money have been minimized.In the best case scenario, with a 6% real return, she’s sitting on a massive 8-figure portfolio 25 years after her retirement, 30 years after she attained FI.That’s more than double what she might have had given the same 6% rate of return had she retired 5 years earlier.

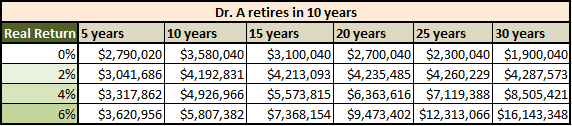

What if Dr. A worked another 10 years beyond attaining financial independence?

At the 10 year mark from her original FI / potential retirement date, she’s got darn near triple what she would have had if she had quit back then.She can expect to be a millionaire the rest of her life, and she can now focus her energies on how to best utilize her oversized nest egg.She is accustomed to a comfortable, but not outlandish lifestyle.But she can easily upgrade from the Ramada to Ritz Carlton without concern.She’s in great shape.

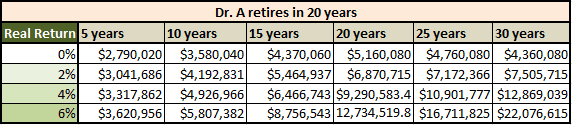

What if she doesn't retire early, and puts in a full 30 years?

Holy Schnikes! Time to contact the alma mater and look into getting your name on a building or two.The Anderson Center for Financial Awesomeness sounds about right.By spending more than most Americans, but less than most physician colleagues, Dr. Anderson can expect to have 20 million dollars or more in her early 70s, after retiring in her early 60s.Simply amazing!

The take-home message?

I think a dozen people could look at the data and come up with 13 opinions.Some will wonder why she didn’t retire a year ago, since she’s got a decent shot at making retirement last under the circumstances.Others will pick their jaw up off the floor after seeing a potential net worth north of $20 million and wonder why anyone in their right mind wouldn’t strive for that.

Personally, I am in a strikingly similar situation to Dr. AndersonLooking at the numbers, another few years seems totally worthwhile.Unless I’m experiencing total burnout, I will gladly continue practicing medicine to better ensure a comfortable future where the likelihood of retirement failure and regret all but disappear.

Would I consider another 20 years?I’ll Never Say Never, but the likelihood is pretty darned low.An absurd net worth is quite possible, but I don’t know what I would do with all that money (besides pay a boatload in taxes).