- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

The US, EU, and Pension Financial Performance

From the Better Finance report regarding EU pension performance, it sounds as if America is not only on the right tract for pension financial reform; we are leading the way!

Clearly, gathering data from EU countries must be like herding cats. They are different in size, gross domestic products, and culture — to name only a few of the disparities. But Better Finance, a public interest non-government group located in Brussels, Belgium, has tried to do just that. It is the only European level organization that is solely dedicated to represent EU individual investors, savers, and other financial service users.

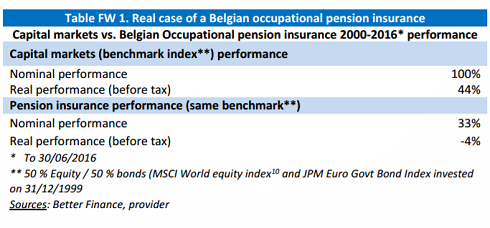

Its findings are shocking. The organization found that those EU members who saved via a pension plan did more poorly, on average, than those who invested their own money. An extreme example is the performance of the Belgian occupational pension insurance fund compared to the capital markets benchmark index (below).

The real performance of the Belgian Occupational pension insurance fund 2000 to 2016 was -4% before tax. For the capital markets benchmark index, defined as 50% equity and 50% bonds (see chart for more detail), it was +44% before tax.

To sum it up, the report stated, “Unfortunately our research findings show that most pension savings did not, on average, return anything close to those of capital markets, and in too many cases even destroyed the real value for European pension savers (i.e. provided a negative return after inflation).” The authors of the report attributed the disparity to high fees and commissions that were not transparent.

To be fair, the average investor rarely performs as well as the benchmark performance to which they are compared. According to a Forbes article, the leading US financial services market research firm, Dalbar, reported that the average American investor in 50% equities and 50% fixed income mutual funds gleaned a 2.6% net annualized rate of return for the 10-year period ending December 31, 2013. Over 20 years, it was 2.5%; and over 30 years, it was 1.9%. So in the US, we have nothing to crow about either. But the important message here is that the US government has successfully reversed any similarity we may have to EU countries where fees and opaque charges diminish any investor return. They did this by passing the Fiduciary Rule, 2016. A fiduciary is someone who has an obligation to act in the interest of another, thereby putting his client’s financial gain above his own.

In the law, the Department of Labor mandated that those who are not now bound by a fiduciary obligation to their 401(k) clients must begin to act in accordance with a fiduciary obligation. In other words, they must act in their customer’s best interests. This means that the product recommended for their customer must not only be appropriate, but also not be the one with the highest commission for the broker or financial professional.

From the Better Finance report regarding EU pension performance, it sounds as if America is not only on the right tract for pension financial reform; we are leading the way!