- Revenue Cycle Management

- COVID-19

- Reimbursement

- Diabetes Awareness Month

- Risk Management

- Patient Retention

- Staffing

- Medical Economics® 100th Anniversary

- Coding and documentation

- Business of Endocrinology

- Telehealth

- Physicians Financial News

- Cybersecurity

- Cardiovascular Clinical Consult

- Locum Tenens, brought to you by LocumLife®

- Weight Management

- Business of Women's Health

- Practice Efficiency

- Finance and Wealth

- EHRs

- Remote Patient Monitoring

- Sponsored Webinars

- Medical Technology

- Billing and collections

- Acute Pain Management

- Exclusive Content

- Value-based Care

- Business of Pediatrics

- Concierge Medicine 2.0 by Castle Connolly Private Health Partners

- Practice Growth

- Concierge Medicine

- Business of Cardiology

- Implementing the Topcon Ocular Telehealth Platform

- Malpractice

- Influenza

- Sexual Health

- Chronic Conditions

- Technology

- Legal and Policy

- Money

- Opinion

- Vaccines

- Practice Management

- Patient Relations

- Careers

To Build Wealth Focus on Savings Not Returns: Part II

While it's true that your savings rate impacts your portfolio more than investment returns, it depends on where you are in your career.

In my last column, I showed you that your savings rate impacts your investment portfolio value far more than investment returns early in your medical career.

However, the impact of the savings rate varies depending on if you’re a mid- or late-career physician.

Mid-career physicians

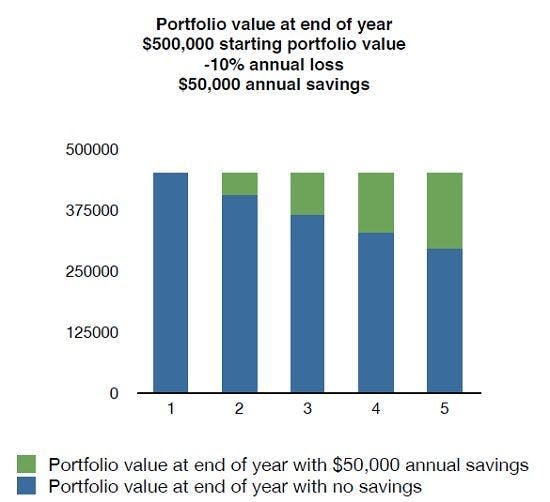

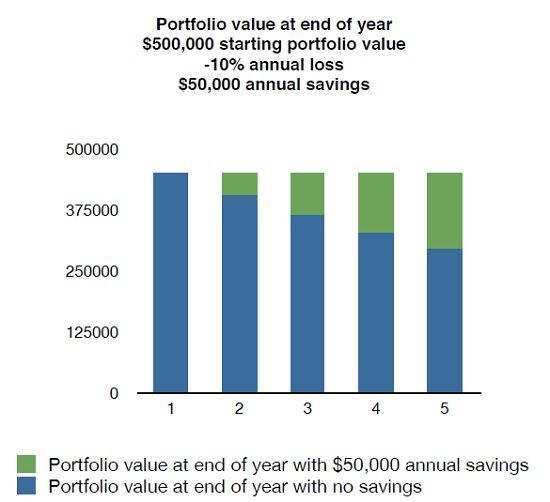

If you’re in the mid part of your career, the math still makes the savings rate rank high. For example, let’s say you have a $500,000 investment portfolio and you save $50,000 a year. Now let’s say the market drops 10%, leaving you with $450,000. Your next contribution of $50,000 brings the portfolio back up to $500,000.

In other words while your investment return was -10%, your portfolio value didn’t lose anything. Your additional savings effectively cushioned the entire loss.

To see what impact your savings have on your portfolio value, take a look at the following chart. The blue bar shows ending annual portfolio values if you start with $500,000, lose -10% annually and don’t save anything. The green bar shows ending portfolio values assuming you contribute $50,000 annually.

Even with a $500,000 portfolio, and assuming a 10% annual gain, your annual savings account for one-third to a half of the gain in your portfolio value.

Late-career physicians

Your investment returns don’t take over savings until you reach higher portfolio values. Suppose you’re 55 years old, still work full time in EM, have an investment portfolio of $2 million, and you’re saving $50,000 annually. Look at the value of your portfolio after two consecutive losses of 10% annually:

Recall that for the mid-career physician, the portfolio value kept going up due to the higher impact of savings, but for the late-career physician, the investment return takes over. While the annual savings provided a little cushion from the investment losses, your portfolio still dropped over $300,000 in value over two years despite your annual savings.

It’s the same way with gains. Starting with $2 million, after two consecutive 10% annual gains, your portfolio value increases by over $400,000, far outpacing the impact of your annual savings.

A great paradox of investing

Herein lies a paradox: To get to higher portfolio values, you have to start with lower portfolio values. And at lower portfolio values, it’s the amount you save that counts a lot more. Only at higher portfolio values do investment returns dominate your portfolio’s change in value.

So instead of focusing on generating high investment returns focus on generating a higher savings rate.